Rev. 6/24

Sales Tax Exemption Administration

Tax Topic Bulletin S&U-6

Contents

Introduction....................................................................................................................................................................... 2

New Jersey Sales and Use Tax Act ....................................................................................................................... 2

New Jersey Exemption Certificates ...................................................................................................................... 2

Streamlined Sales and Use Tax Agreement (SSUTA) .................................................................................... 2

Issuing and Accepting Exemption Certificates ..................................................................................................... 3

Point of Purchase ........................................................................................................................................................ 3

In an Audit Situation.................................................................................................................................................. 4

Unregistered Purchasers .......................................................................................................................................... 4

Drop Shipment Transactions .................................................................................................................................. 5

Use of Blanket Exemption Certificates ................................................................................................................ 5

Retaining Certificates ................................................................................................................................................ 5

Using Exemption Certificates ...................................................................................................................................... 6

Exemption Certificates Available for General Use .......................................................................................... 6

Resale Certificate (Form ST-3) ........................................................................................................................... 6

Resale Certificate for Non-New Jersey Sellers (Form ST-3NR) ............................................................. 9

Exempt Use Certificate (Form ST-4) ................................................................................................................ 9

Streamlined Sales and Use Tax Certificate of Exemption (Form ST-SST) ....................................... 16

Farmer’s Exemption Certificate (Form ST-7) ............................................................................................. 16

Certificate of Exempt Capital Improvement (Form ST-8) ..................................................................... 17

Motor Vehicle Sales and Use Tax Exemption Report (Form ST-10) ................................................. 17

Aircraft Dealer Sales and Use Tax Exemption Report (Form ST-10-A) ........................................... 17

Vessel Dealer Sales and Use Tax Exemption Report (Form ST-10V) ............................................... 18

Contractor’s Exempt Purchase Certificate (Form ST-13) ...................................................................... 18

Exemption Certificate for Student Textbooks (Form ST-16) ............................................................... 19

Exemption Certificates Not Available for General Use .............................................................................. 19

Sales and Use Tax Exemption Certificate (Form ST-4 (BRRAG)) ........................................................ 19

Exempt Organization Certificate (Form ST-5) .......................................................................................... 19

Sales Tax Exemption Administration

Rev. 6/24 2

D

irect Payment Permit (Forms ST-6A and ST-6X) .................................................................................. 20

Contractor’s Exempt Purchase Certificate – Urban Enterprise Zone (Form UZ-4) ..................... 20

Urban Enterprise Zone Exempt Purchase Certificate (Form UZ-5) ................................................... 21

Urban Enterprise Zone – Energy Exemption Certificate (Form UZ-6) ............................................. 22

Salem County – Energy Exemption Certificate (Form SC-6) ............................................................... 22

Connect With Us ........................................................................................................................................................... 22

Introduction

This bulletin explains the most commonly used exemption certificates, the administration of

exemptions, and how and when to use exemption certificates to make qualified exempt

purchases.

New Jersey Sales and Use Tax Act

The New Jersey Sales and Use Tax Act (the Act) imposes tax on receipts from every retail sale

of tangible personal property, specified digital products, specific services, prepared food,

occupancies, admissions charges, and certain membership fees, when the purchaser takes

delivery in this State or the transaction occurs in this State. Under certain conditions,

exemptions are provided for otherwise taxable transactions.

Sellers are required to collect the tax imposed by the Act, unless the seller obtains a fully

completed exemption certificate from the purchaser.

New Jersey Exemption Certificates

The Division of Taxation provides several exemption certificates that are available for general

use by individuals and businesses to purchase taxable goods and services tax-free. Each

exemption certificate has its own specific use. In addition, in most circumstances purchasers

may issue and New Jersey sellers may accept the Streamlined Sales and Use Tax Agreement

Certificate of Exemption (Form ST-SST

) in lieu of the g

eneral use exemption certificates made

available by the Division. The Division also issues exemption certificates that are not available

for general use. These certificates are based on an application and approval process, and the

exemption forms are pre-printed with the taxpayer’s information. Both types of certificates are

described in this bulletin.

Streamlined Sales and Use Tax Agreement (SSUTA)

New Jersey is part of a national coalition of states that conformed their state’s sales and use

tax law to the provisions of the SSUTA. The underlying purpose of the SSUTA is to simplify

and modernize the administration of the sales and use tax laws of the member states in order

to facilitate multi-state tax administration and compliance.

Sales Tax Exemption Administration

Rev. 6/24 3

O

ne of the key principles of the SSUTA is to relieve sellers of tax collection burdens. To

accomplish this, the provisions of the SSUTA hold the seller harmless when a purchaser issues

a fully completed exemption certificate under certain circumstances. A purchaser who claims

an improper exemption is responsible for paying any tax, interest, and penalties.

Issuing and Accepting Exemption Certificates

Point of Purchase

Sellers who accept fully completed exemption certificates within 90 days after the date of sale

are relieved of liability for the collection and payment of Sales Tax on the transactions covered

by the exemption certificate, even if it is determined that the purchaser improperly claimed

the exemption. In this case, the purchaser will be held liable for the nonpayment of the tax.

The following information must be obtained from a purchaser for the exemption certificate to

be "fully completed":

• The purchaser's name and address;

• The type of business;

• The reason(s) for the exemption;

• The purchaser's New Jersey tax identification number, or for a purchaser that is not

registered in New Jersey, the federal employer identification number or registration

number from another state. Individual purchasers must include their driver's license

number; and

• The signature of the purchaser, if a paper or faxed exemption certificate is used

.

T

he seller's name and address are not required and are not considered when determining if

an exemption certificate is fully completed. A seller that enters data elements from a paper

exemption certificate into an electronic format is not required to retain the paper exemption

certificate.

The relief from liability does not apply if a seller fraudulently fails to collect tax, solicits

purchasers to participate in the unlawful claim of an exemption, or accepts an exemption

certificate when the purchaser claims an entity-based exemption when:

1. The subject of the transaction sought to be covered by the exemption certificate is

actually received by the purchaser at a location operated by the seller; and

2. New Jersey has indicated on the Streamlined Sales and Use Tax Agreement Certificat

e

o

f Exemption - New Jersey (Form ST-SST

), that the cla

imed exemption is unavailable.

Sales Tax Exemption Administration

Rev. 6/24 4

In an Audit Situation

If the seller either did not obtain an exemption certificate at the point of purchase, or the seller

obtained an incomplete exemption certificate, the seller has at least 120 days after the

Division’s request for substantiation of the claimed exemption to either:

1. Obtain a fully completed exemption certificate from the purchaser, taken in good faith,

which, in an audit situation, means the seller accepted a certificate claiming an

exemption that:

a. Was statutorily available on the date of the transaction; and

b. Could be applicable to the item being purchased; and

c. Is reasonable for the purchaser’s type of business; or

2. Obtain other information establishing that the transaction was not subject to the tax.

If the seller obtains this information, the seller is relieved of any liability for the tax on the

transaction unless it is discovered that the seller had knowledge or had reason to know at the

time such information was provided that the information relating to the exemption claimed

was materially false, or the seller otherwise knowingly participated in activity intended to

purposefully evade the tax that is properly due on the transaction. The burden is on the

Division to establish that the seller had knowledge or had reason to know at the time the

information was provided that the information was materially false.

Note: For information on the administration of exemption certificates prior to October 1, 2011,

see

Exemption Administration Related to Accepting Certificates

.

Unregistered Purchasers

Purchasers that are not registered with New Jersey must provide one of the following in lieu

of a New Jersey tax identification number when issuing exemption certificates:

• Federal employer identification number of the business; or

• Registration number from another state.

In certain circumstances, a driver’s license number or a foreign ID number may also be

acceptable.

Unregistered purchasers may issue the following exemption certificates:

ST-4

E

xempt Use Certificate

ST-7 Farmer’s Exemption Certificate

ST-8 Certificate of Exempt Capital Improvement

ST-16 Exemption Certificate for Student Textbooks

Sales Tax Exemption Administration

Rev. 6/24 5

Drop Shipment Transactions

When a retailer accepts an order from a New Jersey customer for an item that the retailer has

to purchase from another supplier, and the retailer instructs that supplier to deliver the item

directly to the retailer’s customer rather than to the retailer, this results in a drop shipment. If

the supplier is registered with New Jersey for Sales Tax, the retailer may issue a fully completed

New Jersey Resale Certificate (Form ST-3

) or the Streamlined Sales and Use Tax Certificate of

Exemption (Form ST-SST) to the supplier rather than pay New Jersey Sales Tax on that

purchase. If the retailer is located out of state, the supplier may also accept any of the following

as acceptable proof that the sale to the retailer is a sale for resale:

• P

urchaser’s resale certificate from another state;

• Un

iform Sales & Use Tax Certificate – Multijurisdiction publ

ished by the Multistate Tax

Commission;

• R

esale Certificate for Non New Jersey Sellers (Form ST-3NR);

• Streamlined Sales and Use Tax Certificate of Exemption (Form ST-SST).

Use of Blanket Exemption Certificates

The Division will relieve a seller of the tax otherwise applicable if the seller obtains a blanket

exemption certificate from a purchaser with which the seller has a recurring business

relationship. A recurring business relationship exists when a period of no more than 12 months

elapses between sales transactions. The Division may not request from the seller a renewal of

blanket certificates or an update of exemption certificate information or data elements when

there is a recurring business relationship between the buyer and seller. However, it is

recommended that a seller obtain updated versions every four years to ensure that all

information provided remains accurate.

Retaining Certificates

Sellers must maintain proper records of exempt transactions and provide them to the Division

when requested. All certificates accepted by a seller as a basis for exemption must be retained

by the seller for a period of not less than four years. In addition, individual sales slips, invoices,

receipts, statements, memoranda of price, cash register tapes, or guest checks recording such

sales must be retained for a period of not less than four years from the last date of the

quarterly period for the filing of Sales Tax returns to which individual sales records pertain. All

certificates must be contemporaneously dated, and all supporting documentation must be

retained by the seller.

Summary records are not considered adequate evidence of the accuracy of any exemption

certificate.

For more information, see

Exemption Administration Related to Accepting Certificates.

Sales Tax Exemption Administration

Rev. 6/24 6

Using Exemption Certificates

Exemption Certificates Available for General Use

Resale Certificate (Form ST-3)

Form ST-3 is used by registered sellers to purchase tangible personal property or services

either for resale in its present form or for incorporation into other property held for sale. When

purchasing goods or services, a retailer or wholesaler issues Form ST-3 to the wholesaler or

manufacturer. This exempts the retailer or wholesaler from the Sales Tax on the purchase.

Sales Tax is collected when these items are sold at retail. Businesses registered in New Jersey

may issue Form ST-3 when purchasing the following:

• Inventory intended for resale, rent, or lease

Example

A toy store owner purchases an inventory of dolls to sell on a retail basis. The owner issues

the doll manufacturer a fully completed Form ST-3 instead of paying Sales Tax.

The owner also needs display cases for the dolls. They

may not

use Form ST-3 when

purchasing the display cases because they are not intended for resale. They

must

pay Sales

Ta

x on the display cases.

Example

The owner of an appliance rental store purchases inventory to rent on a retail basis. They

issue their supplier a fully completed Form ST-3 and do not pay Sales Tax on the purchase.

The owner will collect Sales Tax from their customers on the rental charge

.

W

hen items purchased with Form ST-3 are taken out of inventory for personal use, the

business must pay New Jersey Use Tax on the items that are not resold. Use Tax is computed

on the purchase price of the items at the current Sales Tax rate. For more information, see

Use

Tax in New Jersey.

Inventory for resale does not include supplies and materials purchased by contractors.

Contractors (e.g., builders, landscapers)

always

must pay Sales Tax on the materials and

supplies they purchase for installation onto real property unless the materials and supplies are

for exclusive use in fulfillment of a contract with an exempt organization, governmental entity,

a qualified Urban Enterprise Zone business, or a qualified housing sponsor to erect structures,

build on, or otherwise improve, alter, or repair their real property. See

Contractor’s Exempt

Purchase Certificate (Form ST-13)

and

Contractor’s Exempt Purchase Certificate - Urban

Enterprise Zone (Form UZ-4)

for additional information.

NOTE: Fabricator/contractors (i.e., those who build, sell, and install items such as cabinets or

heating ducts that become component parts of real property) and floor covering

dealers follow special rules for paying Sales Tax on materials and supplies.

Sales Tax Exemption Administration

Rev.6/24 7

A

dditional information for contractors, including fabricator/contractors and floor covering

dealers, is contained in

Contractors and New Jersey Taxes

and

Floor Covering Dealers & New

Jersey Sales Tax.

• Raw Materials that will become component parts of the finished product

Example

A silversmith purchases silver to make jewelry. They may issue their supplier a fully

completed Form ST-3 and pay no Sales Tax since the silver becomes part of the jewelry

they are producing for resale.

When they purchase tools for their business, they

may not

use Form ST-3 since the tools

do not become a component part of their finished product. The silversmith must pay Sales

Tax on the tools.

• Services to inventory

Example

A car dealership contracts with a car wash business to provide weekly car washes of the

vehicles that are in its inventory. The dealership may issue a fully completed Form ST-3

and pay no Sales Tax when it purchases the car wash service. This is an expense of the

dealership and would not be charged to the purchaser of the vehicle.

• Services for resale

Example

A gas station cannot complete all the repairs to a customer’s car. The station sends the car

to a transmission specialist who completes the work and returns the car to the gas station.

The gas station may issue a fully completed Form ST-3 to the transmission specialist and

pay no Sales Tax for the parts and services. However, when the gas station bills the

customer, it must charge Sales Tax on the total bill (i.e., the charges for both parts and

labor).

If the gas station has the garage’s hydraulic lifts repaired, it

may not

issue a Form ST-3 to

the repair shop since the service rendered will not be resold. It must pay Sales Tax on t

he

pr

ice of the repair.

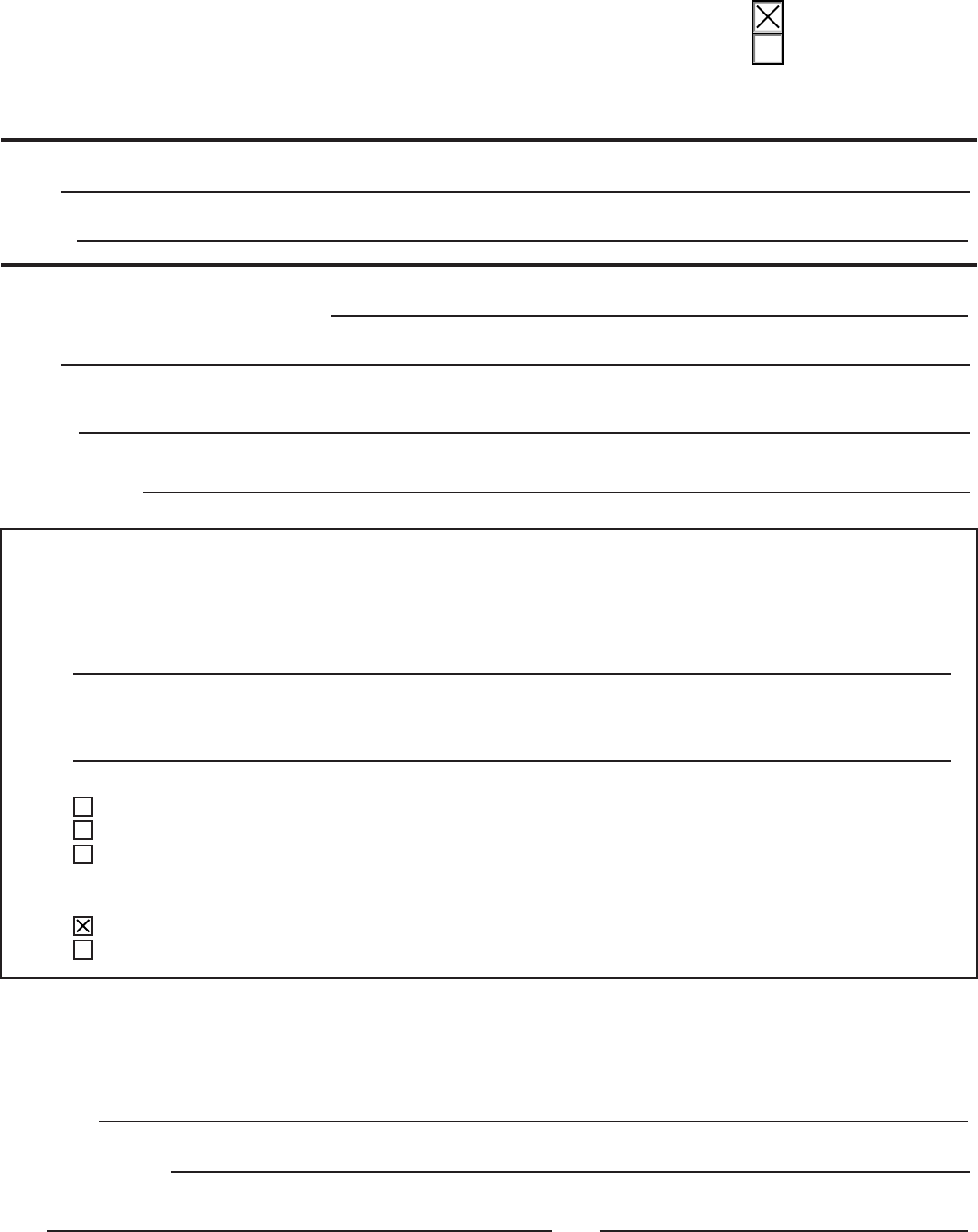

The following is an illustration of how the gas station will complete Form ST-3 issued for

the repair services purchased from the transmission specialist.

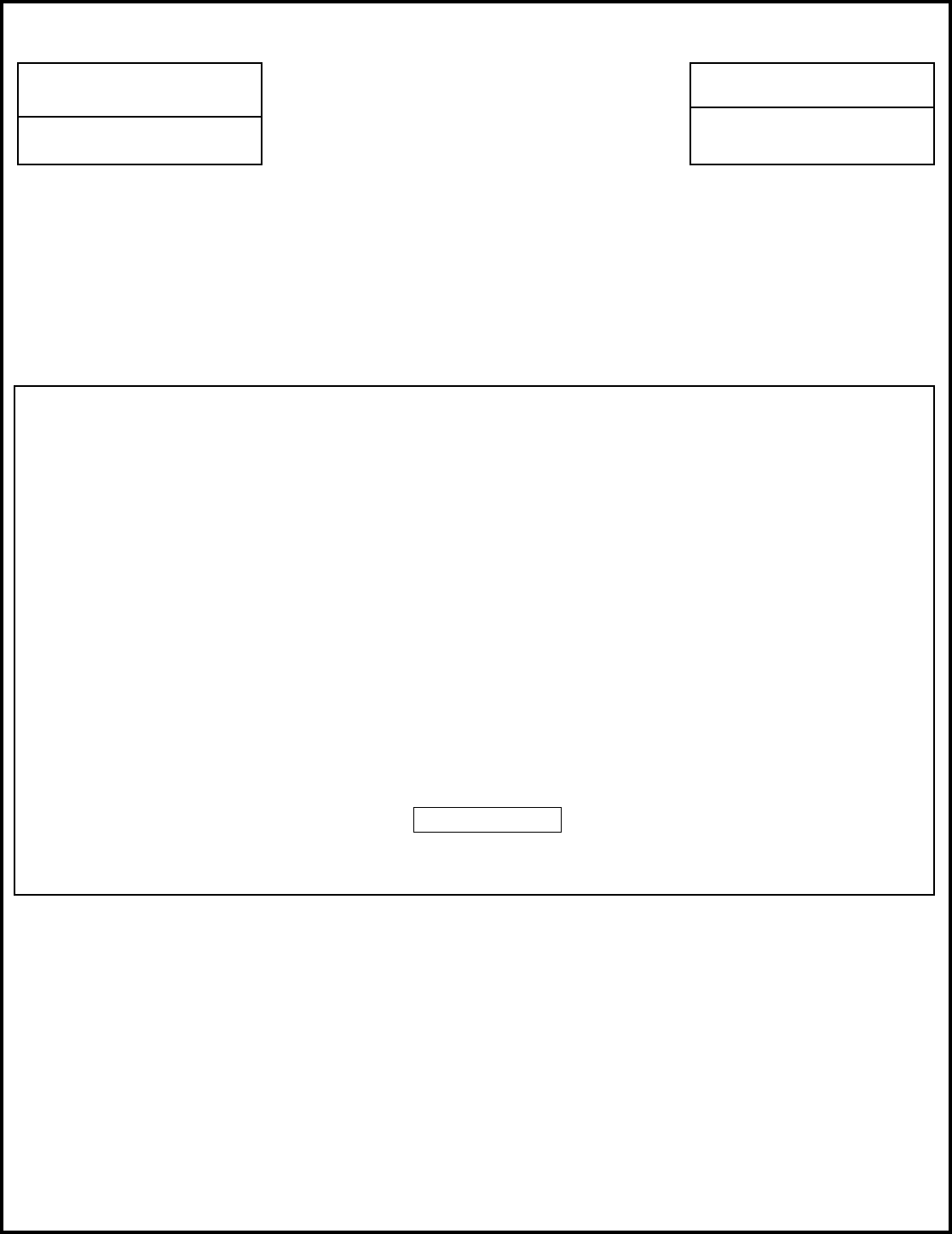

ST-3

(3-23)

New Jersey Division of Taxation

Sales Tax

Resale Certicate

Check applicable box:

Single-Purchase Certicate

Blanket Certicate

The seller must collect Sales Tax on the sale of taxable property or services unless the purchaser gives them a fully completed

exemption certicate.

Do not mail this form to the Division of Taxation.

Seller

Name

Address

Street City State ZIP Code

Purchaser

New Jersey Taxpayer Identication Number

Name*

As registered with the New Jersey Division of Taxation

Address*

Street City State ZIP Code

Type of Business*

The purchaser certies that:

(1) They hold a valid Certicate of Authority to collect New Jersey Sales and Use Tax.

(2) They are principally engaged in the sale of (indicate nature of property or service sold):

(3) The property or services being purchased are described as follows:

(4) The property described above is being purchased for (check all boxes that apply):

Resale in its present form.

Resale as converted into or as a component part of a product by the purchaser.

Use in the performance of a taxable service on personal property and will become part of the property being serviced or will later be

transferred to the purchaser of the service in conjunction with the performance of the service.

(5) The services described above are being purchased (check the box that applies):

By seller who will either collect tax or will resell services.

To be performed on personal property held for sale.

I, the undersigned purchaser, have read and complied with the instructions and rules promulgated pursuant to the New Jersey Sales and Use Tax Act

with respect to the use of the resale certicate, and it is my belief that the seller named herein is not required to collect the Sales or Use Tax on the

transaction or transactions covered by this certicate. The undersigned purchaser hereby swears under the penalties for perjury and false swearing

that all of the information shown in this certicate is true.

Print Name

Authorized Signature*

(Owner, Partner, Corporate Ocer)

Title Date

*Required

This form may be reproduced

Ace Transmission Repairs

163 Holland Ave

Budd Lake

NJ

07828

XXX-XXX-XXX/000

Tom's Gas Station, Inc.

16 Beverly Dr

Budd Lake

NJ

07828

Gas station and mechanic

Thomas Abbott

President

03/01/2023

Sales Tax Exemption Administration

Rev. 6/24 9

R

esale Certificate for Non-New Jersey Sellers (Form ST-3NR)

Form ST-3NR can be used by qualified out-of-state sellers to make tax-exempt purchases in

New Jersey of goods or services purchased for resale. “Qualified out-of-state sellers” are sellers

that (1) are not registered with New Jersey, (2) are not required to be registered with New

Jersey, and (3) are registered with another state.

When a qualified out-of-state seller carries the goods away from the point of sale, or sends

their own vehicle or representative to pick them up in New Jersey, the qualified out-of-state

seller issues a fully completed Form ST-3NR to the seller.

In addition, qualified out-of-state sellers may use a resale certificate for drop-shipment sales

in New Jersey. A drop shipment occurs when an out-of-state seller that is not registered with

New Jersey instructs a New Jersey seller to deliver merchandise to the out-of-state seller’s

customer in New Jersey. For more information, see

Out-of-State Sales

.

Exempt Use Certificate (Form ST-4)

Form ST-4 makes it possible for businesses to purchase certain goods or services performed

on the property without paying Sales Tax if the way they intend to use these items is

specifically exempt under New Jersey law.

In addition to the following qualified purchases, Form ST-4 also may be used by the federal

government, the United Nations, the State of New Jersey and any of their agencies, as

acceptable proof of exemption from Sales Tax when making cash purchases of $150 or less.

The Form can be used instead of an official purchase order or contract.

• Aircraft: Sales of aircraft used by an air carrier engaging in interstate, foreign, or intrastate

air commerce are exempt. The exemption extends to repairs to the aircraft, installation of

equipment or machinery on such aircraft, and replacement parts.

In addition, repairs to aircraft having a maximum takeoff weight of 6,000 pounds or more

as certified by the Federal Aviation Administration, including machinery or equipment

installed on such aircraft and replacement parts, are also exempt. However, the exemption

does not extend to purchases of this class of aircraft.

• Buses: Bus companies whose rates are regulated by the Interstate Commerce Commission

or the Department of Transportation may purchase buses for public passenger

transportation exempt from tax. This exemption also applies to buses purchased by

common or contract carriers that transport children to and from school. Repair and

replacement parts for qualified buses as well as labor charges associated with such repairs

are also exempt.

• Chemicals and Catalysts: Materials used to induce chemical or refining processes in whic

h

t

he materials are an essential part of the process but do not become part of the finished

product are exempt

.

Sales Tax Exemption Administration

Rev. 6/24 10

• V

essels: Commercial ships, barges with at least a 50-ton burden, vessels primarily engaged

in commercial fishing and commercial party boat sport fishing, machinery, apparatus and

equipment used at a marine terminal facility in loading and unloading, and specific services

to, and property purchased for, such vessels are exempt.

• Commercial Motor Vehicles: The purchase, rental, or lease of commercial trucks, tractors,

trailers, and vehicles used in combination with such, that are registered as required by Ne

w

J

ersey law and have a gross vehicle weight rating of more than 26,000 pounds, or ar

e

operated exclusively for the carriage of interstate freight pursuant to federal law are

exempt from tax. Repair parts and replacement parts also are exempt. However, labor

associated with such repairs is not entitled to the exemption. The exemption also applies

to trucks, trailers, and truck-trailer combinations that are used directly and exclusively in

t

he production for sale of tangible personal property on farms when the vehicles have a

gross vehicle weight rating in excess of 18,000 pounds and are registered with the Motor

Vehicle Commission for farm use. The purchaser is not required to be registered with the

State to issue Form ST-4.

Example

A commercial trucker operates a vehicle that is registered in Pennsylvania and has a gros

s

vehicle weight rating in excess of 26,000 pounds. When the trucker has repairs made in

New Jersey, they may issue their mechanic a fully completed Form ST-4 instead of paying

Sales Tax on the parts. Sales Tax must be paid on the charges for labor. As a qualified

nonregistered purchaser, the trucker will enter their FEIN or registration number from out

o

f state on Form ST-4. When they buy motor oil for their truck, they

may not

issue a Form

ST-4. Motor oil is a supply, and Sales Tax must be paid at the time of purchase.

• Commercial Printing: Machinery and equipment used by businesses engaged in

commercial printing, publishing of periodicals, books, business forms, greeting cards, or

miscellaneous publishing, typesetting, photoengraving, electrotyping, stereotyping, and

lithographic platemaking, including supplies are exempt.

• Communications: Telephones, telephone lines, cables, central office equipment, or

station apparatus, or other machinery or equipment, including comparable telegraph

equipment sold to a service provider under the jurisdiction of the State Board of Public

Utilities, or the Federal Communications Commission, for use directly and primarily in

receiving at destination or initiating, transmitting, and switching telephone, telegraph, or

interactive telecommunications service for sale to the general public are exempt.

• Concrete Products that Use Carbon Footprint-Reducing Technology. Receipts from

the sale of unit concrete products that use carbon footprint-reducing technology, which

may include permeable pavement, used in the construction or improvement of any

residential dwelling or commercial building located in New Jersey are exempt.

Sales Tax Exemption Administration

Rev. 8/22 11

• Printed Advertising Material for Use Out of State: Printed advertising material prepared

within or outside of New Jersey by a New Jersey mail house for distribution to recipients

that are out of state is exempt. The exemption applies to charges for printing or production

of printed advertising material whether prepared in New Jersey or shipped into this state

after preparation and stored for subsequent shipment to customers out of state. The

exemption also applies to mail processing services performed in connection with t

he

d

istribution of printed advertising material to recipients out of state. Mail processing

services include, but are not limited to: preparing and maintaining mailing lists; addressing,

separating, folding, inserting, sorting, and packaging printed advertising materials; and

transporting to the point of shipment by the mail service or other carrier.

Example

An advertising agency, located in Trenton, New Jersey, produced a brochure promoting

the products of a leather company in Langhorne, Pennsylvania. The agency also packaged,

labeled, sorted, and mailed the brochure to prospective customers whose names wer

e

s

elected from a mailing list prepared and maintained by the agency. Of the brochures

distributed, 80% were mailed to addresses outside New Jersey. When the agency bills th

e

l

eather company, it must charge Sales Tax on 20% of its fee for printing the brochures

since that is the percentage of printed advertising material that was distributed in New

Jersey. It must also charge Sales Tax on 20% of its fee for the mail processing services

performed in connection with distributing the brochures. Separately stated charges for the

design and layout of the brochure are nontaxable advertising services.

Delivery charges imposed by the seller of a taxable service are subject to tax. Delivery

charges include postage, even if separately stated. Thus, postage charged by the agency

is subject to tax if the processing service is taxable. The agency must charge Sales Tax on

2

0% of the delivery charges based on the percentage of brochures that were distributed

in New Jersey.

If the agency did not perform mail-processing services, but simply produced the brochures

and sent them all to the leather company in Pennsylvania, it would not charge Sales Tax

on the fee for printing the brochures or on the charge for delivering them to the company

since the printed advertising material was shipped to a location outside New Jersey.

• Broadcasting Equipment: Machinery, apparatus, or equipment used directly and

primarily in the production or transmission of radio or television broadcasts by commercial

broadcasters operating under a broadcasting license issued by the Federal

Communications Commission or by providers of cable/satellite television program services

are exempt. The exemption also applies to parts with a useful life of more than one year.

Equipment used in the construction or operation of transmission towers does not qualify

for the exemption.

Sales Tax Exemption Administration

Rev. 6/24 12

• F

ilm/Video Production: Tangible personal property used directly and primarily in t

he

p

roduction of film or video

for sale

including motor vehicles, replacement parts (without

regard to useful life), tools, and supplies is exempt. Charges for installing, maintaining,

servicing, or repairing such property also are exempt. “Film or video” means motion

pictures, including feature films, shorts and documentaries, television films or episodes,

and similar film and video productions whether for broadcast, cable, closed circuit, or unit

distribution, and whether in the form of film, tape, or other analog or digital medium. T

he

ex

emption does not apply to any film or video produced by or on behalf of a corporation

or other person for its own internal use for training, advertising, or other similar purposes.

• Film, Audio/Visual Material: Films, records, tapes, and other types of visual or sound

transcriptions produced for exhibition in theaters or for broadcast by radio or televisio

n

s

tations or networks and not used for advertising are exempt.

• Limousines: Limousines sold to a person licensed under New Jersey law to operate a

limousine service and charges for the repair, including replacement parts, of a limousine

o

perated by a person so licensed or by a person licensed by another state or by the United

States to operate a limousine service are exempt.

A “limousine” is defined as:

1. A

motor vehicle registered under the provisions of N.J.S.A. 39:3-19.5, or registered

as a limousine under the laws of another state or the United States; and

2. Used exclusively in the business of carrying passengers for hire to provide

prearranged passenger transportation at a premium fare on a dedicated,

nonscheduled, charter basis, that is not conducted on a regular route and with a

seating capacity of no more than 14 passengers, excluding the driver.

For purposes of the exemption, a limousine does not include any taxicab, hotel or airport

shuttle or bus, or bus used solely to transport children or teachers to and from school, nor

does it include any vehicle owned and operated without charge by a business entity for its

own purposes.

• Newspaper Advertising: Advertising to be published in a newspaper or magazine, suc

h

a

s display or classified ads, is exempt

.

• N

ewspaper Production Machinery: Machinery and equipment used directly and

primarily in the production of newspapers, including supplies, are exempt if located in the

production department of a newspaper plant.

• Wrapping/Packaging Materials: Wrapping paper, bags, cartons, tape, rope, twine, labels,

nonreturnable containers, and all other packaging supplies

when the use of the supplies

is incidental to the delivery of merchandise

are exempt. Storage containers are not

Sales Tax Exemption Administration

Rev. 6/24 13

c

onsidered to be packaging materials. However, containers used in a farming enterprise

are exempt.

Example

A manufacturer produces television sets. To deliver the sets to wholesalers, the

manufacturer must package them in cardboard boxes and seal the boxes with tape. When

the manufacturer buys the boxes and rolls of tape, it may issue its supplier a fully

completed Form ST-4. However, the manufacturer

may not

purchase the tape dispensers

with Form ST-4 as these items are not part of the packaging used to deliver the television

sets.

The example on the next page illustrates how the manufacturer will complete Form ST-4

when purchasing the packaging materials necessary to deliver its television sets:

I, the undersigned purchaser, have read and complied with the instructions and rules promulgated pursuant to the New Jersey Sales and Use Tax

Act with respect to the use of the Exempt Use Certificate, and it is my belief that the seller named herein is not required to collect the sales or use

tax on the transaction or transactions covered by this Certificate. The undersigned purchaser hereby swears under the penalties for perjury and

false swearing that all of the information shown in this Certificate is true.

__________________________________________________________________________________________

NAME OF PURCHASER* (as registered with the New Jersey Division of Taxation)

__________________________________________________________________________________________

(Address of Purchaser)*

__________________________________________________________________________________________

TYPE OF BUSINESS*

By

__________________________________________________________________________________________

(Signature of owner, partner, officer of corporation, etc.)* (Title)

State of New Jersey

DIVISION OF TAXATION

SALES TAX

FORM ST-4

EXEMPT USE CERTIFICATE

To be completed by purchaser and given to and retained by seller.

Please read and comply with the instructions given on both sides of this certificate.

TO _________________________________________________________________________________ Date _______________________________

(Name of Seller)

________________________________________________________________________________________________________________________

Address City State Zip

PURCHASER’S NEW JERSEY

TAXPAYER REGISTRATION NUMBER

*

The undersigned certifies that there is no requirement to pay the New Jersey Sales and/or Use Tax on the purchase

or purchases covered by this Certificate because the tangible personal property or services purchased will be used for

an exempt purpose under the Sales & Use Tax Act.

The tangible personal property or services will be used for the following exempt purpose*:

The exemption on the sale of the tangible personal property or services to be used for the above described exempt

purpose is provided in subsection N.J.S.A. 54:32B- (See reverse side for listing for principal exempt

uses of tangible personal property or services and fill in the block with proper subsection citation).

MAY BE REPRODUCED

(Front & Back Required)

ST-4 (09-16, R-16)

ELIGIBLE NONREGISTERED

PURCHASER: SEE INSTRUCTIONS

**

*Required

XXX-XXX-XXX/000

West End Packaging

05/19/2021

1166 Homer St Hackettstown NJ 07840

Delivering television sets

8.15

Crest Manufacturing

26 Eleventh Ave Hackettstown NJ 07840

Manufacturing company

President

Sales Tax Exemption Administration

Rev. 6/24 15

• P

rewritten Software for Business Use: Sales of prewritten software delivered

electronically that is used directly and exclusively in the conduct of the purchaser’

s

business, trade, or occupation are exempt. This exemption does not apply to software

delivered by the “load and leave” method or to the purchase of software-related services.

For more information, see Taxability of Software

.

• Production Machinery: Machinery and equipment used directly and primarily in the

production of goods by manufacturing, assembling, processing, and refining are exempt.

The exemption also applies to parts with a useful life of more than one year, and to

imprinting services performed on such machinery. The exemption does not apply to

supplies or to tools that are simple, hand-held, manually operated instruments used in

connection with the production machinery or equipment.

Example

A seller purchases a turret lathe for use in their machine business. The seller may issue its

supplier a fully completed Form ST-4 instead of paying Sales Tax because the lathe will

be

u

sed directly and primarily in the production of goods for sale. However, the seller

may

not

use Form ST-4 to purchase a forklift used exclusively to transport their final product

from the warehouse to the loading dock.

• Recycling Equipment: Equipment that is used exclusively to sort and prepare solid wast

e

f

or recycling or in the recycling of solid waste is exempt. Equipment used in the process

after the first marketable product is produced or equipment used to reduce iron or steel

w

aste to a molten state does not qualify.

• Research and Development: Tangible personal property purchased for use or

consumption directly and exclusively in research and development in the experimental or

laboratory sense is exempt. Research and development in the experimental or laboratory

sense means research and development work which has as its goal or purpose:

1. Basic research in a scientific or technical field of endeavor; or

2. The advancement of technology by experimentation in a scientific or technical field

of endeavor; or

3. The development of new products; or

4. The improvement of existing products; or

5. The development of new uses for existing products.

Research and development does not include the ordinary testing or inspection of materials

or products for quality control, efficiency surveys, management studies, consumer surveys,

advertising, promotions, or research in connection with literary, historical, or other

scholarly research done in fields other than science and technology.

Sales Tax Exemption Administration

Rev. 6/24 16

E

xample

A company purchases materials from which it will construct an apparatus that its research

department will use to test the strength of several new alloys the company is developing.

It will issue a fully completed Form ST-4 to the supplier and not pay Sales Tax on the

purchase since the materials are being used directly and exclusively in laboratory research.

However, it must pay Sales Tax when purchasing the special tools and dies needed to

construct the apparatus since the tools are only incidental to research.

• Solar Energy Devices: Solar energy devices or systems designed to provide heating or

cooling, or electrical or mechanical power by collecting and transferring solar-generated

energy and including mechanical or chemical devices for storing solar generated energy

are exempt.

Example

A New Jersey resident buys a solar energy collector to heat and cool their home. They may

issue the supplier a fully completed Form ST-4 instead of paying Sales Tax on the collector.

However, they

may not

use Form ST-4 to purchase insulation used to reduce heat loss

through their walls, roof, slab, or foundation.

Streamlined Sales and Use Tax Certificate of Exemption (Form ST-SST)

In lieu of the New Jersey exemption certificates, a purchaser may use the Form ST-SST to claim

most exemptions in New Jersey. The purchaser must fully complete the Form according to the

instructions. A New Jersey tax identification number, a federal employer identification number,

a Foreign ID number, or a driver’s license number (for individual purchasers) must be included.

If a valid New Jersey exemption reason is not listed on Form ST-SST, then under Section 5,

“Reason for Exemption,” the purchaser must circle “M” for “Other,” and enter the exemption

basis on the line provided. Some common New Jersey exemptions that are not listed include

recycling equipment, commercial motor vehicles, wrapping/packaging materials, research and

development, and commercial printing. (See

Exempt Use Certificate (Form ST-4)

for additional

information concerning these and other valid New Jersey exemptions.)

Certain entity-b

ased exemptions available in other states might be unavailable in New Jersey.

They are unavailable if the Division of Taxation has grayed out, or crossed out, the exemption

reason type on Form ST-SST. For example, New Jersey law does not provide for a Sales and

Use Tax exemption based on tribal status.

Farmer’s Exemption Certificate

(Form ST-7)

Farmers may issue a fully completed Form ST-7 to purchase goods and certain services used

directly and primarily for the production, handling, and preservation

for sale

of agricultural or

horticultural commodities. The exemption applies only to purchases by the farmer; it does not

apply to purchases by contractors or others doing work for the farmer. A farmer does not need

to be registered with the State to issue Form ST-7.

Sales Tax Exemption Administration

Rev. 6/24 17

T

he exemption does not apply to purchases of automobiles, energy, or materials that will be

incorporated into a building or structure. However, farmers may issue a fully completed Form

ST-7 to purchase materials to construct a silo, greenhouse, grain bin, or manure-handling

facility that is to be used directly and primarily in the production, handling, or preservation of

farm commodities for sale. This exception for certain construction materials applies only to

purchases by farmers. It does not apply to purchases by contractors.

For more information about exempt purchases of certain vehicles registered for farm use, see

Commercial Motor Vehicles

.

Certificate of Exempt Capital Improvement (Form ST-8)

A fully completed Form ST-8 is issued by a property owner to a contractor when work

performed on real property results in an exempt capital improvement. With certain exceptions,

an exempt capital improvement occurs when real property (land or buildings) is improved in

a way that increases its capital value or useful life. A property owner issues a fully completed

Form ST-8 to the contractor and does not pay Sales Tax on the labor portion of the contractor’s

bill. Sales Tax is paid on the materials at the time of purchase by the contractor or by any other

individual making the purchase. A property owner

does

not

need to register with New Jersey

to issue Form ST-8.

For more information, see

Sales Tax and Home Improvements.

Motor Vehicle Sales and Use Tax Exemption Report (Form ST-10)

Form ST-10 is used by registered motor vehicle dealers to report Sales Tax exemptions to the

Division for

nonresidents

who have purchased and taken delivery of motor vehicles in this

State. The purchaser signs Form ST-10 certifying that they are a nonresident and meet all the

requirements for claiming a Sales Tax exemption.

N

OTE: If a person has homes in both New Jersey and another state (e.g., owns a house in New

Jersey, but spends the winters in Florida), they are not entitled to a Sales Tax exemption

as a “nonresident.”

More information on Sales Tax and motor vehicles is available online

.

Aircraft Dealer Sales and Use Tax Exemption Report (Form ST-10-A)

Form ST-10-A is used by registered aircraft dealers to report exempt sales of airplanes. When

a

nonresident

purchases an airplane in New Jersey, no Sales Tax is due provided the purchaser

will base the airplane in another state. If the nonresident purchaser bases the airplane in New

Jersey within 12 months of the date of sale, the exemption is voided, and Sales Tax plus penalty

and interest charges are due on the purchase price of the aircraft.

Sales Tax Exemption Administration

Rev. 6/24 18

V

essel Dealer Sales and Use Tax Exemption Report

(Form ST-10V)

Form ST-10V is used by registered vessel dealers to report exempt sales of boats. An exempt

sale is one made to a New Jersey resident who purchases the boat in New Jersey for use

outside New Jersey and, as part of the sales contract, the dealer transports the boat out of

state, or the dealer arranges to have the boat transported out of state. New Jersey Sales Tax

is due if the resident purchaser does not pay Sales or Use Tax on the boat in another state or

pays tax at a rate less than the New Jersey Sales Tax rate and then subsequently brings the

boat back to New Jersey for use in this state, even on a limited basis.

Also exempt is a sale made to a nonresident who purchases the boat in New Jersey with the

intention of basing it in their state of residence. This exemption applies whether the

nonresident purchaser takes possession of the boat in New Jersey or contracts with the dealer

to have it delivered out of state. If the nonresident purchaser bases the boat in New Jersey

within 12 months of the date of sale, the exemption is voided, and Sales Tax plus penalty and

interest charges are due on the purchase price of the boat. The exemption does not apply if

the purchaser maintains a summer home or other place of abode in New Jersey.

More information on Sales Tax on boats and other vessels is available online

.

Example

A resident of Pennington, New Jersey, purchases a 32-foot motorized sailboat from a

registered vessel dealer located in Toms River, New Jersey. The sales contract specifies that

the dealer will transport the vessel to a marina in Boca Raton, Florida, for use in Florida. The

dealer and purchaser will fully complete a Vessel Dealer Sales and Use Tax Exemption Report

(Form ST-10V), and the dealer will not charge Sales Tax on the transaction.

Contractor’s Exempt Purchase Certificate

(Form ST-13)

Form ST-13 is used by registered contractors to purchase materials, supplies, or services for

use in performing work on the real property of a qualified exempt organization (an

organization that holds a valid New Jersey Exempt Organization Certificate, Form ST-5); or for

a federal or New Jersey governmental entity; or for a qualified housing sponsor. The contractor

must contract directly with the exempt entity in order for the exemption to apply. The

contractor issues a fully completed Form ST-13 to their supplier and does not pay Sales Tax

on the purchase price, provided the materials will be entirely used or consumed on the job.

Form ST-13 must include the exempt organization number shown on Form ST-5 or, if the work

is being done for a qualified government entity, the entity’s purchase order or contract

reference number.

Form ST-13

may not

be used to rent machinery or equipment or to purchase tools or materials

such as hammers and tarpaulins (rain covers) that may be used on other jobs. For more

information, see

Contractors and New Jersey Taxes

.

Sales Tax Exemption Administration

Rev. 6/24 19

E

xemption Certificate for Student Textbooks

(Form ST-16)

The sale of textbooks for use by students in a school, college, university, or other educational

institution, approved as such by the State Department of Education, is exempt from Sales Tax.

When the educational institution indicates the books are required reading for school

purposes, the purchaser may issue the seller a fully completed Form ST-16 and

does not

pay

Sales Tax. The purchaser

is not

required to be registered with New Jersey to issue Form ST-16.

Exemption Certificates Not Available for General Use

Sales and Use Tax Exemption Certificate (Form ST-4 (BRRAG))

The New Jersey Economic Development Authority administers the Business Retention and

Relocation Assistance Grant Program, which includes a Sales and Use Tax exemption on the

purchase of “eligible property” for certain businesses relocating and retaining jobs within New

Jersey. Form ST-4 (BRRAG) is issued to these businesses and can be used by both the business

and its contractors to purchase eligible property to be incorporated into or used at the

location listed on the form.

Exempt Organization Certificate (Form ST-5)

A Form ST-5 is issued by the Division to a qualified, registered nonprofit organization, which

can use the Certificate to purchase, with its own funds, most goods and services for its

exclusive use without paying Sales Tax. Some examples of organizations that may have exempt

status are churches, hospitals, veterans’ organizations, and fire companies. When making

purchases, the organization gives the seller a photocopy of its Form ST-5 in lieu of paying

Sales Tax.

A seller may only accept a copy of Form ST-5, which has the name, address, and registration

number of the exempt organization imprinted on the Certificate by the Division of Taxation,

along with the signature of the Division Director.

When Form ST-5 is not applicable. Although qualified nonprofit organizations are exempt

from New Jersey Sales Tax, these organizations are not exempt from the State Occupancy Fee

or the Municipal Occupancy Tax for renting a hotel room or a transient accommodation. Thus,

Form ST-5 may not be used to exempt a qualified nonprofit organization from paying either

the State Occupancy Fee or the Municipal Occupancy Tax.

Form ST-5 also is not applicable to purchases of energy (natural gas and electricity).

Governmental Exemption. Form ST-5 is not required for the United States or State of New

Jersey departments or agencies, or New Jersey political subdivisions or public schools to make

tax-exempt purchases. Payment from government funds with the official letterhead or a

purchase order signed by a qualified officer is sufficient proof of exemption for the seller. A

fully completed Form ST-4 signed by a qualified government or school official is satisfactory

for cash purchases of less than $150.

Sales Tax Exemption Administration

Rev. 6/24 20

T

here is an exemption from paying the State Occupancy Fee and the Municipal Occupancy

Tax for agencies and instrumentalities of the United States and the State of New Jersey, and

New Jersey political subdivisions and public schools. Documentation provided to exempt

purchases from Sales Tax is also sufficient to provide exemption from the State Occupancy

Fee and the Municipal Occupancy Tax.

For more information, see

Tax Treatment of Nonprofit Organizations and Government Entities

.

Direct Payment Permit (Forms ST-6A and ST-6X)

An application for a Direct Payment Permit may be filed only by registered businesses that

acquire tangible personal property or services under circumstances that make it impossible at

the time of purchase to determine the taxable status of the property or services.

To obtain a Direct Payment Permit, an Application for Direct Payment Permit (Form ST-6B)

must be completed and mailed to:

New Jersey Division of Taxation

PO Box 287

Trenton NJ 08695-0287

NOTE: The holder of a Regular Direct Payment Permit may not use Form ST-6A to purchase

property or services that are clearly taxable at the time of purchase, such as office equipment

and supplies, repair services, etc.

The holder of a valid Audit Direct Payment Permit may issue Form ST-6X at the time of

purchase according to the terms of the taxpayer’s audit agreement governing use of the

Certificate.

A list of Direct Payment Permit Holders is available online

.

Contractor’s Exempt Purchase Certificate – Urban Enterprise Zone (Form UZ-4)

A contractor issues a fully completed Form UZ-4 to suppliers when purchasing materials that

will be incorporated into real property, supplies that will be entirely used or consumed on the

job, or services for use in performing work for a qualified business at the business’s real

property in an Urban Enterprise Zone. The contractor must contract directly with the qualified

business in order for the exemption to apply. The exemption does not apply to equipment

that the contractor rents or leases to perform work for a qualified business. The contractor can

only obtain Form UZ-4 from a qualified business. The contractor also issues copies of Form

UZ-4 to subcontractors for their use in making exempt purchases for the job. Subcontractors

must attach their name, address, and Sales Tax Certificate of Authority number (in addition to

the name, address, and number of the contractor) and then give the UZ-4 and attachments to

their sellers. This Certificate is not available to businesses located within Urban Enterprise

Zone-impacted business districts.

Sales Tax Exemption Administration

Rev. 6/24 21

Beginning January 1, 2022, only the first $100,000 in taxable purchases of construction

materials, supplies, and services made by all contractors hired to work on a qualified business’s

property in a calendar year are exempt from Sales and Use Tax. Once all contractors’ annual

taxable purchases on behalf of a qualified business total $100,000, that qualified business may

no longer give the UZ-4 to contractors or subcontractors for the remainder of that calendar

year. At that point, a qualified business should advise contractors and subcontractors that it

may no longer use a UZ-4 to make exempt purchases for the remainder of that calendar year.

More information on Urban Enterprise Zones is available onlin

e.

Urban Enterprise Zone Exempt Purchase Certificate (Form UZ-5)

Under the Urban Enterprise Zones Act, a qualified business is entitled to an exemption from

Sales and Use Tax on purchases of taxable tangible personal property (other than motor

vehicles and motor vehicle parts and supplies) and taxable services (except

telecommunications services)

for exclusive use or consumption on the premises of the

qualified business at its zone location

. This exemption does not apply to purchases of gas and

electricity used by the qualified business at its zone location unless the business is a qualified

Urban Enterprise Zone manufacturer that meets specific eligibility requirements. [See “Urban

Enterprise Zone — Energy Exemption Certificate (Form UZ-6)” below]. Only personal property

controlled by the qualified business qualifies for the exemption.

Tangible personal property includes items such as construction materials, office supplies,

office or business equipment, office and store furnishings, trade fixtures, cash registers, etc.

Exempt services performed for a qualified business at its zone location include items such as

janitorial and maintenance services, installing, maintaining, or repairing tangible personal

property used in business, etc.

Beginning January 1, 2022, only the first $100,000 of taxable purchases in a calendar year are

exempt from Sales and Use Tax. Once a qualified business reaches its annual $100,000 exempt

purchase limitation, the business must cease using a UZ-5 and pay Sales Tax on any

subsequent business purchases for the remainder of the calendar year. If a qualified business

is over its annual exempt purchase limitation and a supplier does not charge the required

Sales Tax on a taxable transaction, Use Tax

m

ust be remitted for that purchase.

Supermarkets and grocery stores located in a food desert community or within an Urban

Enterprise Zone are not subject to the annual $100,000 exempt purchase limitation. In

addition, supermarkets and grocery stores located within an Urban Enterprise Zone but

outside of a food desert community must receive an annual certification from the New Jersey

Department of Community Affairs to be eligible for the unlimited tax exemption.

In order to document the exemption, the qualified Urban Enterprise Zone business provides

its supplier with a fully completed copy of its Form UZ-5. The transaction must be completed

Sales Tax Exemption Administration

Rev. 6/24 22

by

delivery within the effective dates on the UZ-5. This Certificate is not available to businesses

located within Urban Enterprise Zone-impacted business districts.

More information on Urban Enterprise Zones is available online

.

Urban Enterprise Zone – Energy Exemption Certificate (Form UZ-6)

The Form UZ-6 is issued to UEZ-certified manufacturers that meet the New Jersey Economic

Development Authority’s program employment requirements established under the Business

Retention and Relocation Assistance Act.

To qualify, the manufacturer must employ at least 250 people within the zone, at least 50% of

whom are employed directly in the manufacturing process. The Certificate applies to the

business’s purchase of natural gas, electricity, and the transportation and transmission of both

commodities, and must be renewed annually.

A list of Urban Enterprise Zone – Energy Exemption Certificate holders is available online

.

Salem County – Energy Exemption Certificate (Form SC-6)

The Form SC-6 is issued to Salem County-certified manufacturers that meet the New Jersey

Economic Development Authorities program employment requirements established under the

Business Retention and Relocation Assistance Act.

To qualify, the manufacturer must employ at least 50 people within the zone, at least 50% of

whom are employed directly in the manufacturing process. The Certificate, which applies to

the business’s purchase of natural gas, electricity, and the transportation and transmission of

both commodities, must be renewed annually.

A list of Salem County – Energy Exemption Certificate holders is available online

.

Connect With Us

Email your State tax questions;

Visit a Regional Information Center;

Call (609) 292-6400;

Subscribe to our NJ Tax Alert E-News;

Follow us on: